Last week CIMSEC featured a series of pieces submitted in response to our call for articles on maritime infrastructure and trade, issued in partnership with Maersk Line, Limited as a part of Project Trident.

Authors highlighted the dynamic and ever-evolving nature of the global maritime system. A burgeoning volume of maritime trade and commercial vessels is traversing the world’s oceans and driving globalization to new heights. Maritime infrastructure is being upgraded time and time again in a bid to keep pace. But as the global community reaps the benefits of maritime exchange, the scope of threats is becoming more multi-faceted.

The deep interconnectedness of global maritime infrastructure is paralleled by the close connectivity of its cyber dimensions. Cybersecurity for maritime facilities remains a point of concern for global shipping firms and those who depend on their supply chains. Meanwhile, efforts to decarbonize maritime infrastructure, especially shipbuilding, will lend themselves toward an uneasy transition away from traditional fuel sources. China’s globe-spanning efforts to invest and procure maritime infrastructure is raising eyebrows and underscoring the nation’s commitment to becoming a global maritime superpower. The question of how China could use these assets to employ coercive leverage remains a concern. And as the blockage caused by the Ever Given demonstrates, an incident involving a single ship in a critical maritime space can grab headlines, choke off billions in trade, and send far-reaching disruptions into economies.

While threats are changing and the maritime system is rapidly growing, an important constant endures. Growing global prosperity is inseparable from maritime infrastructure and trade, and careful tending of the maritime system will prove indispensable for continued human progress.

Below are the authors who featured during the topic week. We thank them for their excellent contributions.

“This U.S. mandate is a hard law, both clear and enforceable. To meaningfully address known cybersecurity vulnerabilities across the world’s port facilities, the member states of the IMO should collaborate and amend Part A of the ISPS Code to include a similar mandate. By hardening the law in this way, member states can establish a consistent, uniform enforcement framework and thus, begin to harden port facilities against cyberattacks.”

“…the security-related risks of the United States pursuing decarbonization merit further scrutiny, especially with respect to decarbonization’s impact on the shipbuilding industrial base and its ability to contribute in a protracted great power conflict.”

“The People’s Republic of China (PRC) has embarked on a massive investment spree and established a meaningful stake in the control of global maritime infrastructure…There is growing concern that the PRC has, or could, use its investments to deny infrastructure access to its rivals.”

“Major powers are never going to be able to significantly alter the ratio of warships to commercial vessels, so they must seriously revisit the strategy for how the protection of trade is conducted in peace and in conflict.”

“… ships traveling between Europe and Asia piled up in the anchorages off Port Said and Suez, hoping that the Suez Canal Authority, and eventually SMIT Salvage, could clear the containership and allow a resumption of normal trade. Her removal after six days opened the floodgate of vessels looking to traverse the canal and resume the international flow of goods and allow military vessels…to perform their missions. But behind the veneer of memes and jokes the grounding of Ever Given exposed the fragile nature of global trade and the maritime infrastructure that supports it.”

Dmitry Filipoff is CIMSEC’s Director of Online Content. Contact him at Content@cimsec.org.

Featured Image: The Port of Los Angeles (Photo by Michael Justice)

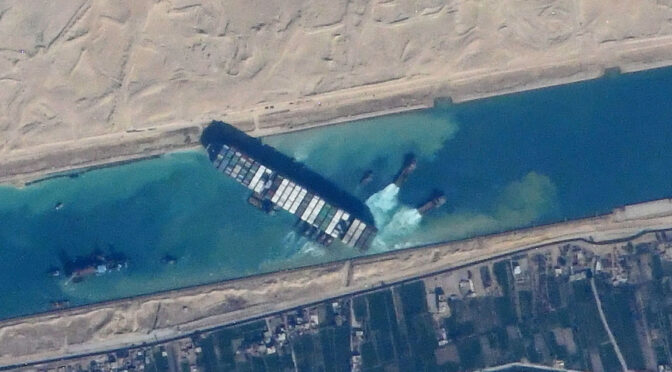

The grounding of MV Ever Given from March 23 to March 29, 2021 captured the world’s attention. Many people asked, how could such a modern and large vessel find itself with its bow rammed into Asia, its stern aground on Africa, and its midship astride one of the major maritime chokepoints in the world? The world was also entertained with thousands of images from the little digger scratching away at the sand along the ship’s bow, to a representation of Austin Powers trying to dislodge Ever Given from a tunnel. Amidst all of this, ships traveling between Europe and Asia piled up in the anchorages off Port Said and Suez, hoping that the Suez Canal Authority, and eventually SMIT Salvage, could clear the containership and allow a resumption of normal trade. Her removal after six days opened the floodgate of vessels looking to traverse the canal and resume the international flow of goods and allow military vessels – such as the USS Dwight D. Eisenhower carrier strike group – to perform their missions. But behind the veneer of memes and jokes the grounding of Ever Given exposed the fragile nature of global trade and the maritime infrastructure that supports it.

The Ever-Growing Containership

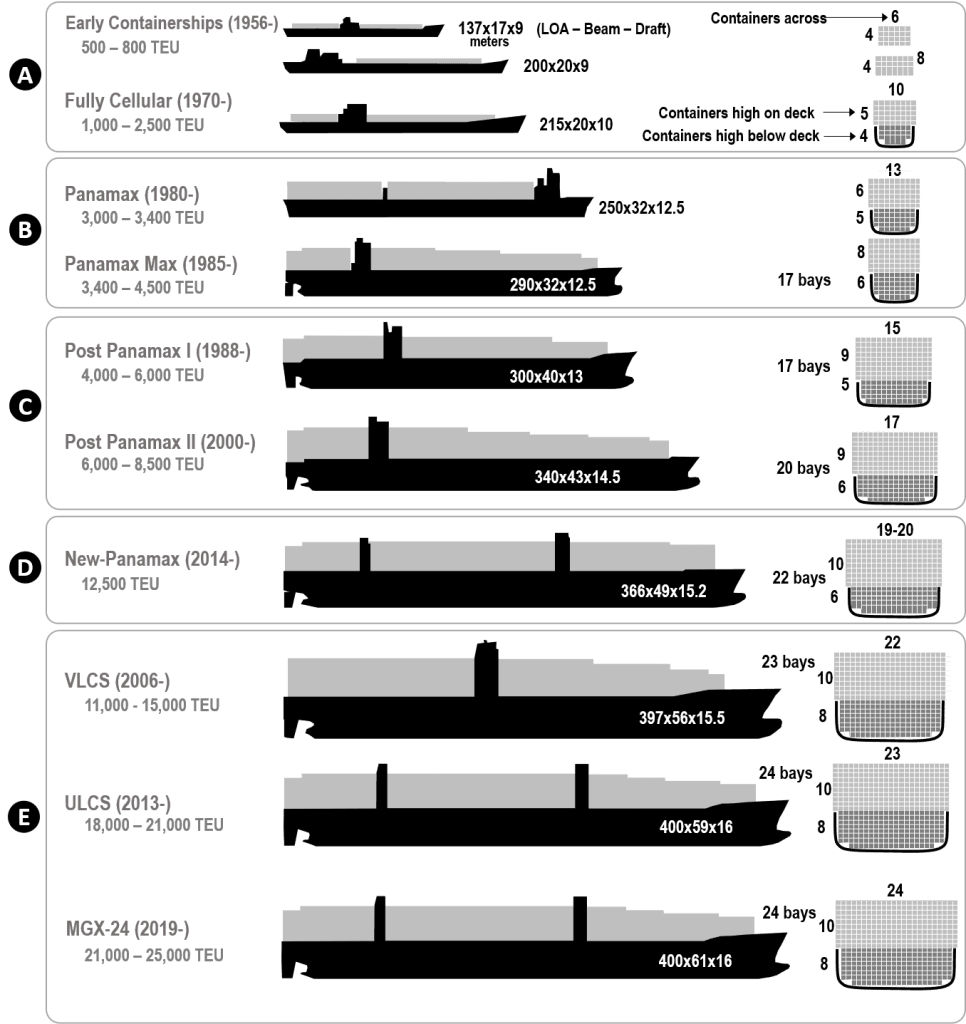

One of the many questions asked following the event concerned the size of Ever Given. At 1,300 feet in length, 200 feet across, drawing nearly 48 feet of water, with a deadweight capacity of 200,000 tons, and capable of carrying 20,000 twenty-foot equivalent units (TEUs), she is one of the largest ships in the world. Part of a new generation of Ultra Large Container Ships (ULCSs), these behemoths were ushered into the world when Maersk Lines introduced their new Triple E-class in 2011. Touted for their Economy of Scale, Energy Efficiency, and Environmentally improved, the ships were 1,309 feet long and 193 feet wide, and they could not transit the Panama Canal – including the new lane opened in 2016. They were capable of speeds of 22 knots and could carry 18,000 containers. By comparison, when the first containership, SS Ideal X, was introduced in 1956 by Malcolm McLean, she could only carry 58 boxes. A little over a half a century later, this had expanded over 300-fold. This was necessary as world maritime trade boomed from 880 million tons in 1956 to 8,775 million tons in 2011. Today it peaks at over 11 billion tons daily.

Container ships not only carried more cargo, but they improved all aspects of the process, from loading, to movement via truck or rail, to ports, stowage aboard ships, offloading, and transportation to the consignee. During World War II, an American Liberty ship had the ability to transport 10,000 tons of cargo. It would take days, or even weeks, to individually load, block and brace individual cargo within the holds of the ships. Sailing at a speed of 11.5 knots, once they arrived, it took nearly as much time to unblock and unstow the cargo. The Triple Es could move twenty times the cargo, faster and more efficiently with a fraction of the crew. It is difficult to definitively answer the question if the ULCSs were built to support the increase in world trade, or if the ULCSs facilitated the growth themselves.

Prior to the Triple Es, McLean, and his company Sea Land, along with Maersk, continually pushed the envelope of containership construction. In 1972, McLean introduced the SL-7s, which at 33 knots were the fastest cargo ships in the world. Unfortunately, the timing for their operation coincided with the OPEC embargo and the skyrocketing cost of fuel. This ultimately led to Sea Land selling the ships to the U.S. Navy for conversion into Fast Sealift Ships. Today the eight ships, approaching their 50th anniversary, remain as elements of the aging Maritime Administration Ready Reserve Force. Maersk adopted a more conservative approach to speed and focused on carrying capacity with the introduction of their L-class in 1980. At 24 knots and able to carry 3,400 containers, almost three times that of the SL-7s, the Ls marked the first of several innovative jumps in containership size over the next few decades. Ironically, the L-class would also end up with the U.S. Navy after the Persian Gulf War when converted into the Shughart-class roll-on/roll-off ship for the Military Sealift Command.

February 02, 2007. Army Strykers make their way down the USNS Shughart’s gangplank. (Wikimedia Commons)

Concurrently, McLean, then at the helm of United States Lines in the early 1980s built a dozen large vessels intended to inaugurate an around-the-world service. Capable of carrying 4,258 boxes, the Econships built by Daewoo in Korea were the flagships of the American merchant marine, but suffered from one serious shortfall. Learning his lesson from the SL-7, McLean opted for fuel efficiency and carrying capacity over speed. The ships were agonizingly slow at 16 knots. A new competitor, Evergreen Marine, appeared on the scene and offered a similar around-the-world service, with both east and westbound service, and faster vessels. This tradeoff between cargo capacity and speed could only be overcome by increasing the overall size of the vessel. Maersk accomplished this by introducing the R-class in the early-1990s (6,000 TEUs), the S-class in the late-1990s (8,000 TEUs), the E-class in the mid-2000s (12,500 TEUs) and then the Triple Es in the early 2010s (18,000).

The roll out of the Triple Es was a master performance by Maersk. They invited the world’s maritime press and influencers to Korea for the launch of Maersk McKinney Moller. Concurrently, the Discovery Channeldeveloped a multi-episode series on the vessel. Maersk even had fellow Danish company Lego unveil a set featuring the vessel. The construction of the 20 vessels also highlighted another vital aspect of world maritime infrastructure: shipyards.

When Malcolm McLean built his SL-7s, he went overseas to Germany and the Netherlands since he did not want to be constrained by construction and differential subsidies available under the Merchant Marine Act of 1936. Similarly, he built the Econoships in Korea. Most Maersk ships were built in their own yard in Denmark, Odense Steel Shipyard, but following the global recession of 2008, Maersk closed the facility. In February 2011, Maersk contracted with Daewoo Shipbuilding and Marine Engineering to build 10 ships for $1.9 billion. A few months later, in June, they exercised an option for an additional 10 for a similar price. Maersk McKinney Moller was handed over to the company from Daewoo on July 2, 2013. The last of the twenty, Mathilde Maersk, followed on June 30, 2015. A total of 20 ships were launched in two years and four months, a mindboggling delivery schedule.

A look at a list of the ULCSs reveals that they follow the trend of world ship construction today where over 90 percent of all commercial ships are built in either Japan, the Republic of Korea, or the People’s Republic of China. Except for the Philippines, with about four percent, the remaining six percent is spread around the world with no other nation having a single percentage of construction. In many ways, the demise of commercial shipping in the United States and across Europe, along with the economic recession of 2008, and the need to further expand on the size of ships like the Triple Es, promoted the shipbuilding race between these three East Asian countries. Like the dreadnought race of the early twentieth century, these three nations are aligning their shipyards into larger entities to outbid, outproduce, and outlast those of their neighbors.

Evolution of containerships [Click to Expand] (Graphic via Transportgeography.org) In 2015, Maersk followed up with Daewoo and ordered eleven 2nd generation Triple Es, each capable of carrying over 20,000 containers. Passing that mark led to a full-on competition between the major carriers, including COSCO, Evergreen, ONE, CMA CGA, Mediterranean Shipping Company and HMM, fielding 77 ships, with follow-on orders on the book for an additional 56 ULCSs with ships capable of carrying up to 24,000 boxes included in the mix. Of the nine major container lines, which possess 82.7 percent of the world container capacity, none are American-owned or flagged and are structured into three large alliances – 2M, The Alliance and the Ocean Alliance – which dominate the world’s trade routes.

As the vessels continue to grow, the infrastructure to support them must adjust to accommodate them. Along the East Coast of the United States, cities and states undertook massive dredging projects to allow entry of these larger containerships, but not the ULCSs as they could not navigate the new lane of the Panama Canal. This required dredging down to 50 feet and in the case of New Jersey, raising the height of the Bayonne Bridge to permit vessels to pass underneath. That cost was borne by the citizens of those communities for ships registered and owned overseas and cargo being distributed throughout the nation. The chasing of infrastructure goals may have been what caught up with Ever Given in the Suez on March 23.

Regardless of the cause, the closing of the canal marked an important event not just in the world economy but the shipment and protection of trade. While the event was over quickly, a long-term closure, such as what happened during the Suez Crisis or the Six Days War, would have global ramifications. The vulnerability of the chokepoint to an accident, and now the efforts by the Egyptians to extract $916 million from Evergreen for the event, may cause companies and nations to reconsider their use of the canal. One nation looking at the incident in a positive light is Russia. Their attempts to entice cargo into the Arctic and utilize the Northeast Passage may now appear a more viable solution, although some firms, such as MSC, indicate they are not interested.

For China, their concern over the closing of their sea lanes of communication has been the paramount reason for the growth of the PLA Navy and their efforts to develop bases in the South China Sea and Indian Ocean, astride their major trade routes. Taking the writings of Alfred Thayer Mahan literally, they realize that the role of the military is to support their economic endeavors, protect the supply of raw materials – such as bulk material from South America, Africa, and Australia – and exports of their finished products.

It is noteworthy that while China has appeared to have learned this lesson from history and the recent past, the United States fails to heed this concern. America lags in infrastructure, as the repeated announcements by presidents of infrastructure bills and programs indicate. The current backlog of containerships off the West Coast, particularly the ports of Los Angeles and Long Beach are not so much an issue with the ports but the ability to get the cargo off the terminals via road and rail and into the interior of the United States – which was the precise issue that Malcolm McLean attempted to alleviate with the advent of containerization in the 1950s.

March 29, 2021 – A satellite image shows parts of the traffic jam adjacent to the Suez canal caused by the Ever Given’s obstruction. [Click to Expand] (Photo via Wikimedia Commons)The military learned this lesson during the Vietnam War, when Sea Land was contracted to provide eleven containerships to alleviate a similar backlog of breakbulk ships. The commercial sector viewed the success in the Vietnam War as validation. In the Persian Gulf War, while ammunition was shipped much as the Phoenicians did in ancient times – in separate bundles and packages – the Military Sealift Command contracted with seven American firms to ensure there was enough container capacity between the continental U.S. and Southwest Asia to support military forces. A little over a decade later, with the adoption of the Maritime Security Program to ensure that a fleet of U.S. flagged vessels were available, along with the vast networks of many of the companies, such as Maersk, American ships were able to sustain Department of Defense forces throughout the wars in Afghanistan and Iraq.

However, today the infrastructure and trade of the United States is in peril. Failure to incorporate the commercial maritime sector into national defense planning documents and provide visible and vocal support is undercutting the industry. Ships that make up the afloat prepositioning force, the surge sealift, and the domestic Jones Act fleet need replacement as they are aging.Investment into national shipbuilding would have an impact on military vessel construction by employing more workers into this industry instead of the boom-and-bust cycle which requires repeated training and loss of experience. An examination of Chinese shipyards reveals commercial ships being built alongside new frigates, destroyers, and aircraft carriers.

It is strange to see the world’s fleets building vessels larger than Ford-class carriers and competing in trade that at one time was being battled over by national fleets. Today, international corporations, with ships flying the flags of open registries, dominate the world’s oceans but with little means of protection. This is readily apparent to the Indian crew, onboard the Taiwan-based Evergreen vessel, managed by a German firm, with an American classification society, owned by a Japanese company, with insurance in Great Britain, and trapped in Egyptian waters. That is the situation facing world trade and maritime infrastructure today that is largely absent from most military and naval discussions but essential to the world’s economy and the military’s logistics. Failure to invest in domestic infrastructure and trade will place nations at the mercy of forces beyond their control. While that may be sufficient for many nations, any country wishing to be considered a sea power should heed the words of Mahan, as recently recapped by Andrew Lambert in “What is a Navy For?” and consider, “What is a Merchant Marine For?”

Salvatore R. Mercogliano is a former merchant mariner, having sailed and worked ashore for the Military Sealift Command. He is an associate professor of history at Campbell University and an adjunct professor at the U.S. Merchant Marine Academy. He has written on U.S. Merchant Marine history and policy, including his book, Fourth Arm of Defense: Sealift and Maritime Logistics in the Vietnam War, and won 2nd Place in the 2019 Chief of Naval Operations History Essay Contest with his submission, “Suppose There Was a War and the Merchant Marine Did Not Come?”

Featured Image: The containership Ever Given stuck in the Suez Canal in Egypt, viewed from the International Space Station. (Photo via Wikimedia Commons)

In his authoritative tome Seapower, Geoffrey Till observes that navies “have to work alongside rather than regard themselves as distant from and somehow superior to many other maritime stakeholders with their grubby little concerns.” Mariners indeed need to be “all of one company,” as Drake recommended.”1 As the world’s navies dramatically shrink relative to the ever growing fleets of commercial shipping cousins, they should take time to understand their fellow maritime stakeholders and make themselves “all of one company.” Major powers are never going to be able to significantly alter the ratio of warships to commercial vessels, so they must seriously revisit the strategy for how the protection of trade is conducted in peace and in conflict.

Navies and Commercial Shipping

Since humanity devised methods for crossing bodies of water (starting with rivers and lakes, then seas and oceans), people have been carrying items from one side to another as gifts, or offerings, to barter and trade. This symbiotic movement is synonymous with the development and emergence of civilizations, and the building of great nations like the United States and China. Today, more than 80 percent of all trade is moved by sea, which makes seaborne trade a crucial backbone of the global economy and human progress.

In comparison to the thousands of years of continuous commercial seaborne exchange, formal standing navies are relative newcomers. For centuries the principal reason for having a navy was to protect merchant ships from criminal activity, like piracy. It was the maritime explorer kingdoms of Portugal and Spain that established the first standing navies, followed by the burgeoning northern European trading nations. King Henry VIII’s break with Rome and the dissolution of almost a thousand wealthy monasteries funded the building of what would become the British Royal Navy in the 16th century. From their inception, navies have been intrinsically linked to the economic development of a country, and in England “The navy served the City of London, not the crown.”2 Similarly, the U.S. Navy was initially formed to defend U.S. trade passing through the Mediterranean against Barbary pirates from North Africa. According to Lincoln Paine’s excellent book, The Sea and Civilisation, the forming of a naval force was based on the “naval-commercial complex” 3 being the dominant characteristic of economic growth from maritime expansion.

Despite most democratic maritime nations listing “protection of trade” or similar phrases within their core purposes of maritime strategy, it seems that this driver is often overshadowed by political maneuvering, demonstrating that “The modern world takes the free use of the seas for granted and assumes shipping services are wholly detached from national policy.”4

It is useful to look at the composition of the modern maritime space. The principal driver behind commercial shipping fleet size and shape is derived demand5 driven by the consumer. As the global population continues to swell and the worldwide consumer class grows, the demand for manufactured goods, foods, and fuel increases at a voracious rate. The requirement for more vessels carrying cargo, moving passengers, catching and processing seafood, extracting and producing fossil fuels, mining rare metals and blue biotechnology from the ocean and seabed increases rapidly.6

A Burgeoning Maritime Space

Today, around 1.6 million seafarers crew the 98,140 oceangoing cargo vessels, carrying over 11 billion tons of cargo, including 811.2 million twenty-foot equivalent units (TEU) containers handled worldwide, and passing through more than 5,250 ports.7,8 There are 4,428 passenger-carrying ships (cruise ships and ferries),9 around 4.6 million fishing vessels (including artisanal, coastal and ocean going),10 and approximately 25 million11 pleasure craft across the world in 2019. This makes for extremely complex and dynamic global trade routes and coastal areas.

The increasing demand for new cargo ships ensures a busy shipbuilding industry, which in 2019 launched a staggering 66 million GT of new shipping, which is the equivalent tonnage of roughly 660 U.S. Nimitz-class aircraft carriers.12,13 Almost all new merchant ships are constructed in East Asia (China 40 percent, Republic of Korea 25 percent, and Japan 25 percent), whilst the remaining 10 percent of ships are built in shipyards across the rest of the world.14

By comparison, the main naval powers’ fleets are shrinking.15 While systems, sensors, and weapons are undeniably more capable, the ratio between the number of naval platforms available to protect sea lanes and the quantity of commercial vessels is becoming more and more disproportionate.

Applying Lessons Learned

There was a glimpse of how the interaction between navies and commercial shipping can work very successfully for a specific problem, providing some valuable lessons. During the period of Somali piracy (2008-2012), three separate international naval coalitions were established, demonstrating unprecedented cooperation and collaboration between different navies to counter the piracy threat. Additionally, the naval coalition commanders, and leaders of the shipping industry and marine insurance industry formed the Senior Leadership Forum, which held periodic meetings at a naval headquarters near London to discuss strategic and policy issues related to Somali piracy.

From late 2008 the naval coalitions and shipping industry worked together in the quarterly Shared Awareness and Deconfliction (SHADE) Group meetings in Bahrain, allowing all parties to discuss the operational situation with naval commanders in the region. At the tactical level, the Royal Navy’s UK Maritime Trade Operations (UKMTO) organization provided a “911” first responder-type service to merchant ships entering the Western Indian Ocean, briefed masters’ and crews visiting UAE ports, and assisted with the coordination of maritime forces when piracy attacks happened.

The formation of these tiered levels of liaison and interaction between the naval coalition forces and the shipping industry paved the way to the suppression of Somali piracy by mid-2012. The structure was also regarded by many senior naval officers as a fascinating and edifying experience to work closely with their shipping industry counterparts, demonstrating the benefits of viewing elements of maritime power as “all of one company.” The downside to the achievements of this successful model was that it was possibly too short-lived for the valuable lessons to be fully inculcated and applied more broadly.

Conclusion

As we move further into what is being called the maritime century, it is inevitable that interaction between navies and the shipping industry will become more common, whether it be through state-on-state friction, piracy and armed robbery at sea, maritime terrorism, or mass maritime migration. It is therefore important that both naval officers and the shipping industry better understand each other. Both organizations should include within their respective trainings new educational periods and liaison visits to understand their maritime counterparts. This closer relationship would engender a far greater understanding and appreciation of each other’s ethos, outlook, concerns, and fears. A closer relationship created over time will build trust, and hopefully induce the conditions for naval forces and the commercial shipping industry to become “all of one company.”

Peter Cook is a former Royal Marines Officer and spent a significant part of his 24-year career involved in different aspects of maritime security, including from maritime counterterrorism to formulating counterpiracy policy and procedures for the UK Ministry of Defence. In 2011 he developed the concept and was the co-founding CEO of the Security Association for the Maritime Industry (SAMI), the representative body for the global private maritime security industry. SAMI was at the epicentre of defining international and commercial standards for private armed guards onboard commercial ships in the fight against Somali piracy. In 2016, he was co-founder of PCA Maritime, a maritime security consultancy, which serves UNODC, major shipping associations, flag States, and marine insurers. Having attained a MSc in Maritime Operations and Management at City, University of London in 2018, he is a visiting lecturer to several universities internationally on the evolving discipline of maritime security. He is an Associate of the Corbett Centre for Maritime Policy Studies, King’s College London and Honorary Fellow at the Australian National Centre for Ocean Resources and Security (ANCORS) University of Wollongong. Peter is also the Managing Editor of the International Journal of Maritime Crime and Security (www.ijmcs.co.uk).

References

[1] Seapower A Guide for the twenty-first century TILL p416

[2] Seapower States, LAMBERT p237

[3] The Sea and Civilization PAINE p5

[4] Seapower States LAMBERT p328

[5] Derived demand is driven by three factors; cargo type, shipping operation and commercial philosophy; Maritime Economics 3rd Edition STOPFORD p568

[6] Over the past four decades more than 50,000 natural compounds have been reported from marine-derived organisms that could support the production of a range of chemicals, foods and antibiotics, many previously unknown.

[7] United Nations Conference on Trade and Development Review of Maritime Transport 2020 p37

The People’s Republic of China (PRC) has embarked on a massive investment spree and established a meaningful stake in the control of global maritime infrastructure. These investments include the construction of new ports, the expansion and modernization of cargo handling facilities, the purchase of port management rights, and the establishment of control over the operations of petroleum storage and transshipment depots. Much of the capital is formally sourced from the PRC’s One Belt One Road Initiative, but major investments are also being made directly by state-owned, PLA-linked, and other Chinese enterprises. The scope of control over global maritime infrastructure has become sufficiently large to be of concern. The U.S. Navy’s 2021 Chief of Navy Operations NAVPLAN warns that China is, “extending their infrastructure across the globe to control access to critical waterways.“1

There is growing concern that the PRC has, or could, use its investments to deny infrastructure access to its rivals. To date, PRC enterprises have not overtly denied access to others, but they are creating business models that advantage their partners over their commercial competitors. These advantages could have acute impacts for rivals should colluding PRC enterprises be able to establish themselves as a maritime infrastructure cartel or monopolize a specific market segment. However, PRC investment will have to grow considerably more before either of these options available. In contrast, infrastructure investments are already an important element of the PRC’s growing geo-economic influence over its partners. What deserves greater attention is the implications of PRC investments in global maritime infrastructure by specifically focusing on questions involving the potential denial of competitors’ infrastructure access.

The Scope of PRC Investments in Global Maritime Infrastructure

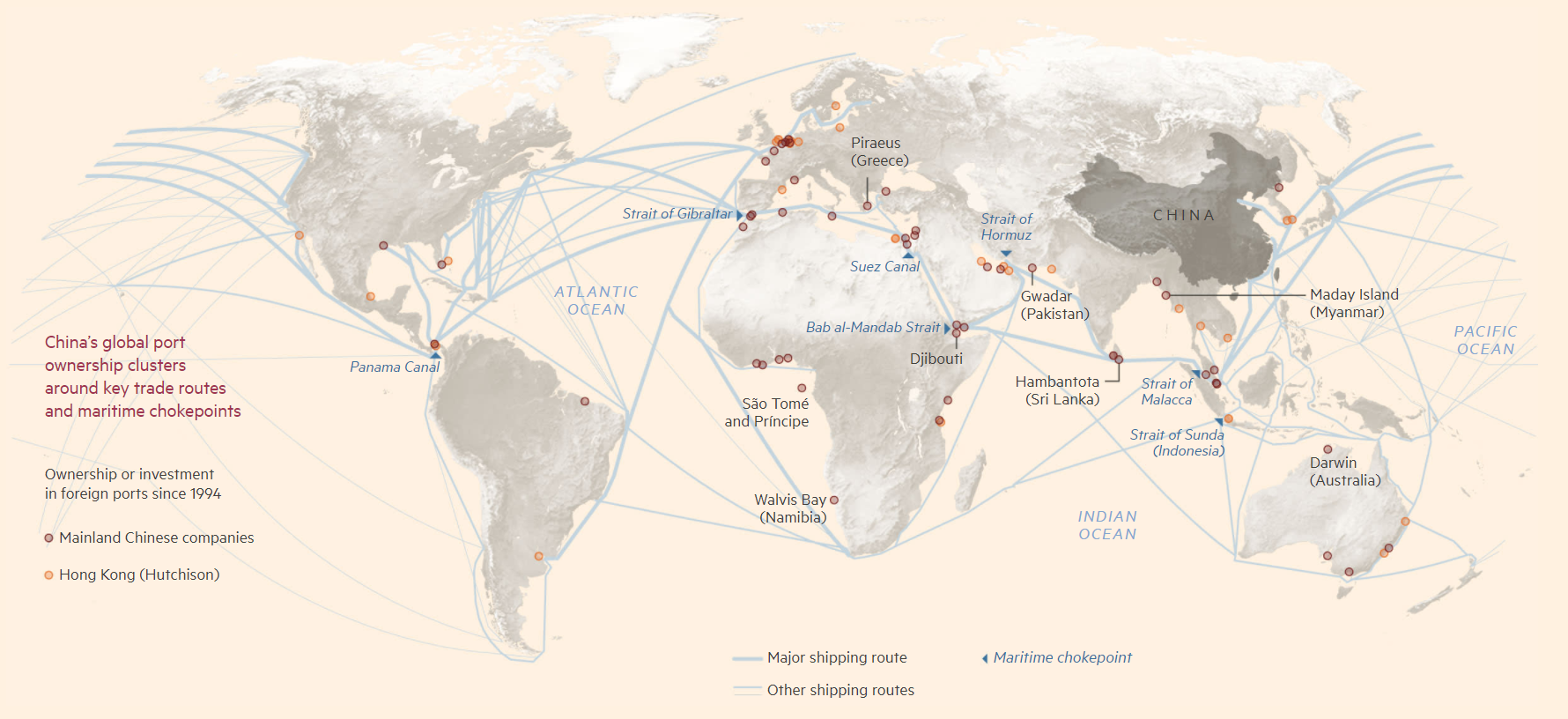

The infrastructure investments in question are distributed globally and concentrated along the PRC’s main trading routes. The most well-discussed examples along the PRC’s Maritime Silk Road that stretches across the Indian Ocean to Europe include Koh Kong (Cambodia), Melaka (Malaysia), Kyaukpyu (Myanmar), Hambantota (Sri Lanka), Gwadar (Pakistan), Doraleh (Djibouti), and Piraeus (Greece). Looking south and east from China, high-visibility examples include Darwin (Australia); Asua (Solomon Islands); and Luganville (Vanuatu). The chain of PRC maritime infrastructure investments also reaches across the Mediterranean (e.g., Venice, Italy; Tangier, Morocco, and Valencia, Spain), north into Europe (e.g., La Havre, France, Odessa, Ukraine, and Zeebrugge, Belgium), and across the Atlantic (e.g., Freeport, Bahamas and Colon, Panama). Especially noteworthy are the investments around key maritime chokepoints. Colon is at the Caribbean entrance to the Panama Canal. The PRC is also playing a key role in the development of Egypt’s Suez Canal Economic Zone while COSCO Shipping Port company owns a minority share of Suez Canal Terminal.2

The extent of this investment spree is sufficiently large that it is difficult to catalog. Dr. Geoffrey Gresh of the U.S. National Defense University notes that two-thirds of the world’s top 50 container ports have received PRC investments.3 In 2019, Hong Kong-based Hutchinson Port Holdings was the world’s second-largest container port operator, running more than 50 terminals worldwide. Third place COSCO Shipping Ports runs fewer ports but handles more total cargo. China Merchant Ports Holding operates nearly 40 ports in around 20 countries.4

Click to expand. China’s global port investments. Ports in China and Hong Kong not shown. Includes investments announced and completed. (Graphic via the Financial Times. Sources: King’s College, London; FT research; CIA (shipping routes))

Other PRC firms staking out control over global maritime infrastructure include China Harbor Engineering Company, Qingdao Port International Development, Shanghai International Port Group, the Ningbo-Zhoushan Port Company, Dalian Port Corporation Limited, the Guangxi Beibu Gulf International Port Group, the Shenzhen Yantian Port Group, and the Rizhao Port Group. The AEI/Heritage Foundation China Global Investment Tracker, one of the largest public databases to register this sort of PRC activity, includes over 100 investments in the shipping subsector that total around $2 trillion U.S. dollars. This does not include maritime infrastructure investments filed into the database under categories such as construction, logistics, or energy.5

A great deal of analysis examines the impact of these investments on the naval balance of power. The U.S. government has been clear in its concerns. For example, the U.S. Department of Defense’s 2020 China Military Power Report notes that the PRC concept of Fundamental Domain Resource Sharing dictates that these maritime infrastructure investments are required to provide dual-use functionality and will have important implications “as the PRC seeks to establish a more robust overseas logistics and basing infrastructure to allow the PLA to project and sustain military power.”6 The report specifically states that the PRC has probably already made overtures toward the establishment of such military logistics facilities in Namibia, Vanuatu, and the Solomon Islands, and has likely considered Myanmar, Thailand, Singapore, Indonesia, Pakistan, Sri Lanka, United Arab Emirates, Kenya, Seychelles, Tanzania, and Angola.7 The December 2020 U.S. tri-service maritime strategy similarly warns: “Chinas One Belt One Road initiative is extending its overseas logistics and basing infrastructure that will enable its forces to operate farther from its shores than ever before, including the polar regions, Indian Ocean, and Atlantic Ocean. These projects often leverage predatory lending terms that China exploits to control access to key strategic maritime locations.”8

In comparison to the military aspects, much less reporting and analysis are openly available regarding the commercial implications of the PRC’s global maritime infrastructure investments. There are anecdotes and rumors about PRC-connected port management companies denying access to other nations’ shipping, but this research project was not able to credibly verify these reports. This seems to be because the PRC-related managers are not overtly denying access. Instead, they establish business structures and rules that advantage PRC shipping and thereby force the others to select alternate routing options. These advantages could come in the form of price structures, prioritization for berths, expeditious filing of entry permits and other paperwork, and other measures. These sorts of business advantages would be especially available when the port operator is the same firm as the shipper (e.g., COSCO), but can be assumed to create conditions generally favorable to all PRC operators.

The Strategic Elements of PRC Investments in Global Maritime Infrastructure

The centralized nature of the PRC systems would indicate that, while its various overseas maritime stakeholders do not move in absolute synchronicity, they act with support from the national government and under some degree of strategic direction from the Chinese Communist Party. COSCO, Chinese Merchants, and other large state-owned enterprises have CCP committees embedded into their management boards.9 However, this is not to argue that all investments are part of a centrally-driven master plan. Nor should the sum of the investments be viewed as a monolithic strategy. Often the maritime infrastructure investments are ad hoc investments or independently viable business opportunities that may involve foreign investments moving through the Chinese firms.10

While the linkages between the commercial enterprises, the military, the banking sector, and the state enables Chinese intra-national collusion to become more effective, other global maritime infrastructure stakeholders also take advantage of similarly coordinated cross-sector positions. For example, the vertically integrated Maersk family of Danish businesses includes both the world’s largest shipping company and, with 76 ports in 41 countries, the globe’s fifth-largest port operator.11 Providing a clear example of public-private linkage, the world’s largest port operator, PSA International, is directly tied to the Singapore government.

A growing concern is that continued expansion of PRC investment may enable its vertically integrated enterprises to collude to gain sufficient market share necessary to establish a global maritime supply chain cartel. This could undermine the current advantages of other major players, raise global costs, and create access issues for non-PRC shippers. However, the development of such a market share is far from a foregone conclusion. In fact, a Drewry senior analyst argued that the risk has been disproportionately reported and generally overstated. He points out that, “In the Asia region, Chinese terminal operators accounted for a quarter of all throughput in 2018, but their presence is far more limited in the rest of the world.”12

The degree to which PRC enterprises collude against non-Chinese players is also unclear. The major shipping alliances that enable slot-sharing and vessel-sharing agreements between the largest carriers are not assembled along national lines.13 In August 2020, PRC authorities opened an investigation into whether COSCO (a Chinese company) might be colluding with Maersk, MSC, CMA CGM, Hapag Lloyd, and Evergreen (all non-PRC enterprises) to inflate trans-pacific shipping prices. Similarly, in 2017 the U.S. Department of Justice also raided the biannual Box Club meeting in San Francisco, delivering subpoenas to the assembled CEOs of major international container lines as a part of an anti-trust investigation that involved Chinese and non-Chinese firms. The U.S. closed that investigation in 2019 without prosecutions.14

Regardless of the parties involved, the United States would be particularly disadvantaged if faced with collusion among maritime supply chain participants because of its reliance upon foreign enterprises. The United States no longer has a significant ownership stake in the shipping sector. COSCO carries about 70 times as much cargo as Matson, the largest U.S. carrier.15 The largest U.S. port operator, SSA Marine, has a global reach, operating ports on every continent except Europe, but its total throughput is less than one-third that of China Merchant Ports, one-sixth of Hutchinson or COSCO, and one one-seventh of PSA International.16

PRC government backing is a key enabler of China’s drive for dominance in the maritime infrastructure sector. For example, the opportunity for COSCO to invest in Zeebrugge opened when Maersk’s APM decided to pull out of the relatively small, low-profit port. The concession agreement likely prevented the port’s closure and the retrenchment of its staff. While the agreement was formerly made with COSCO, there is no doubt about the influential role of the PRC government.17 In 2018 the PRC Ambassador to Belgium addressed the bilateral group of government and private industry leaders gathered to conclude the deal by explaining, “The launch of Belt and Road initiative between China and Belgium in 2014 has laid a solid foundation for today’s signing ceremony.”18 In 2019 Zeebrugge enjoyed a growth rate of more than 14 percent thanks to its new role as COSCO’s northern European hub.19

Other PRC investments have been more acrimonious. PRC government loans were essential to enabling COSCO to establish a controlling stake and make investments valued at around $8 billion in Piraeus, Greece.20 The port’s throughput increased significantly because of increased handling capacity, improved connectivity, and the subsequent reshaping of regional trade patterns.21 However, local resentment grew as established workers were fired or put on reduced wages.22

Sept. 6, 2019 – A cargo ship of COSCO Shipping Lines transporting Italian products for the 2019 China International Import Expo (CIIE) to Shanghai berths at the Port of Piraeus, Greece. (Photo by Lefteris Partsalis/Xinhua)

In other cases, the PRC-backed projects have received more problematic resistance. In the early 2000s, the PRC invested hundreds of millions of dollars to finance the expansion of Pakistan’s Gwadar Port. In 2007, PSA International took a 40-year concession to build and operate that port, but immediately faced issues regarding the specific terms of the agreement and the security of the facilities. After only five years, PSA transferred the contract to China Overseas Port Holdings.23 Pakistani Information Minister Qamar Zaman Kaira explained, “PSA could not develop or operate Gwadar ‘as desired.’ The Chinese will make ‘more investment’ to make the port operational.”24 Although Gwadar’s facilities remain under-utilized and unprofitable, it has grown as a focal point for PRC activities in Pakistan. The initiatives include more port construction, the inauguration of a Sino-Pakistan economic free zone (from with China received 85 percent of the profits), and $800 million in Chinese pledges for projects to support the local population such as the construction of a school, expansion of a hospital, and improvement of the public water treatment system.25 Violent separatists began targeting Chinese workers around the port as early as 2004 and the violence is intensifying. The Balochistan Liberation Army (BLA) attacked the Chinese consulate in Karachi in 2018 and in 2019 three BLA members stormed Gwadar’s Pearl Continental Hotel, killing five people.26 In the wake of these incidents, the PRC is doubling down on its presence by financing the fencing off of over 60km2 around the seaport.27

The PRC’s commitment to Gwadar demonstrates that the maritime infrastructure investments are driven by more than a simple desire to expand the profitability of China’s international trade. Indeed, while Gwadar may someday become a profitable commercial hub, it seems likely to bring even greater benefit to the PRC as a naval staging area or as an economic anchor holding Pakistan in the PRC’s geopolitical orbit. In fact, Gwadar and other investments are specifically designed to carry geo-economic weight.

A useful academic definition of geo-economics is, “the use of economic instruments to promote and defend national interests and to produce beneficial geopolitical results; and the effect to other nations’ economic actions on a country’s geopolitical goals.”28 Maritime infrastructure investments are particularly powerful geo-economic instruments for several reasons. First, their scale is such that they convey a lot of capital and that equates to a lot of immediate influence, especially with the investor that can control the rate of disbursement.29 Furthermore, the investments are such that they create recurrent sources of wealth in the form of on-sight labor requirements, maintenance requirements, and international trade. However, to a greater extent than other infrastructure (for example, interior roads or schools), maritime infrastructure binds the port community to China. Once the investments are complete, the new or enlarged facilities are reliant on trade to stay active. In extreme cases, the ‘Port-Park-City’ model is employed. Development of the port is followed by a Chinese-funded/managed industrial park, and then the emergence proxy Chinese city.30 However, the investment does not bind China by reciprocal dependency; if the port state were to deny access to PRC shipping, the PRC can rely on its diversified portfolio to reroute shipping via other infrastructure.

The Keys to Controlling Port Access

There is no clear case where the PRC has overtly exercised its geo-economic power to deny competitors port access. However, such a situation is far from unimaginable. The PRC has overtly used its geo-economic leverage, much of which is tied to its investments in Piraeus to persuade Greece to weaken EU statements denounce the PRC’s human rights effort.31 There are also unconfirmed rumors that the PRC has quietly used its influence to arranged for denial of access to Japanese ships.32 In contrast, U.S. Navy ships continue to call in Piraeus.33 While overt action to prevent access would incur costs such as political backlash and increased insurance costs, the PRC will likely expect those costs to diminish as its relative power expands.34 Therefore, should the PRC be faced with a crisis or the appropriate pressures, it would not be surprising if it sought to exercise this option.

The concept of using infrastructure investments to create international leverage is not new. One study explained that “China is updating and exercising tactics used by Western powers during the nineteenth and twentieth centuries.”35 More specifically, the denial of access to maritime infrastructure to achieve political aims is well-established in international relations. These tools have been used by states and the international community in recent years.

United Nations Security Council (UNSC) Resolutions against North Korea currently restrict that nation’s access to global maritime infrastructure. In October 2017, the UNSC took the unprecedented action of banning four ships accused of smuggling North Korean coal from entering any port. In April 2018, the Wise Honest, one of North Korea’s largest cargo ships, was detained in Indonesia and then seized by the United States. When a local Indonesian court allowed the cargo from the Wise Honest to be released, it was loaded onto the ship Dong Thanh operated by Qingdao Global Shipping. Because of its illicit cargo and the use of associated falsified documents, Dong Thanh was denied entry to Malaysia before it called into Vietnam.36 U.S. government cited authorities found in domestic legislation when seizing M/T Courageous, another vessel smuggling oil to North Korea, that has been held in port by Cambodian officials since March 2020.37

The clearest example of a state currently unilaterally acting to prevent another state from accessing maritime infrastructure is recent U.S. sanctions on Iran. The sanctions have been enacted through domestic U.S. legislation and have the stated aim of denying Iran the financial resources to support terrorist organizations and other armed factions, or to further its nuclear and weapons of mass destruction programs. These sanctions do not require other countries to impound any Iranian ships or other cargo, but in September 2019, guidance was updated to state that port bunkering services for Iranian oil shipments could subject firms and individuals to U.S. sanctions.38 Unilateral U.S. sanctions have also created challenges for Iranian shippers to obtain insurance, since a New York-based pool of insurance organizations, the International Group of P&I Clubs, dominates the shipping insurance industry.39

Conclusion

The PRC’s rapidly expanding network of global maritime infrastructure investments is already delivering meaningful commercial advantages. Further expansion of this network could bring it sufficient additional leverage that it can impede rivals’ ability to freely operate. Active collusion between PRC enterprises would make their power particularly problematic. However, the market still appears sufficiently competitive to prevent this from becoming an immediate concern. In the near term, a larger worry is that these maritime infrastructure investments will provide the PRC with sharp geo-economic power to influence the behavior of partner nations. While using that power to deny access to a competitor would come with certain costs, it seems completely plausible that, given the proper incentives, the PRC could consider pushing a port state to take such an action.

John Bradford is a Senior Fellow in the Maritime Security Programme at the S Rajaratnam School of International Studies and the Executive Director of the Yokosuka Council on Asia Pacific Studies. Prior to entering the research sector, he spent 23 years as a U.S. Navy Surface Warfare Officer focused on Indo-Pacific maritime dynamics.

References

[1] M. Gilday, CNO NAVPLAN, Jan 2021 <https://www.navy.mil/Press-Office/Press-Releases/display-pressreleases/Article/2467465/cno-releases-navigation-plan-2021/#.YIERS3QoZiU.link>

[2] Claudo Ferrai and Alessio Tei, “Effect of BRI strategy on Mediterranean shipping transport,” Journal of Shipping and Trade, 5:14, 2020, p. 12 and Jevans Nyabiage, “Why China is banking on Suez and plans for a new Egyptian capital,” South China Morning Post, 10 Apr 2021 <https://www.scmp.com/news/china/diplomacy/article/3129000/why-china-banking-suez-and-plans-new-egyptian-capital>

[3] Geoffrey Gresh, To Rule Eurasia’s Waves: The New Great Power Competition at Sea, London: Yale University Press, 2020, p. 11

[4] “Top 10 Box Port Operators 2019,” Lloyd List, 01 Dec 2019 <https://lloydslist.maritimeintelligence.informa.com/LL1130163/Top-10-box-port-operators-2019> and Gresh, p. 65

[5] China Global Investment Tracker <https://www.aei.org/china-global-investment-tracker/>

[6] U.S. Department of Defense, China Military Power Report 2020, p. 19.

[7] U.S. Department of Defense, p. 120.

[8] U.S. Department of the Navy, Advantage at Sea, p. 4.

[9] Charles Lyons Jones and Raphael Veit, Leaping Across the Ocean: The port operators behind China’s naval expansion, Australian Strategic Policy Institute, pp. 4, 8, 14 and 25.

[10] Ferrai and Tei, p. 7.

[11] “Top 10 Box Port Operators 2019;” Jones and Veit, p. 10; and “Biggest shipping companies: Top ten by TEU capacity,” Ship Technology <https://www.ship-technology.com/features/the-ten-biggest-shipping-companies-in-2020/>

[12] James Baker, “Chinese ownership of foreign ports concerns are ‘overstated’, Lloyds List, 03 Dec 2019 <https://lloydslist.maritimeintelligence.informa.com/LL1130247/Chinese-ownership-of-foreign-ports-concerns-are-overstated>

[13] “Newly Formed Ocean Alliance has Huge Impact on Container Shipping,” Atlas Logistics Network <https://atlas-network.com/newly-formed-ocean-alliance-has-huge-impact-on-container-shipping/> and Ocean Alliance, JOC.com <https://www.joc.com/maritime-news/container-lines/ocean-alliance>

[14] Costas Paris, “U.S. Drops Container Shipping Cartel Investigation Without Charges, Wall Street Journal, 26 Feb 2019 <https://www.wsj.com/articles/u-s-drops-container-shipping-cartel-investigation-without-charges-11551200327>

[15] Matt Woodley, “Top 30 International Shipping Companies,” MoverFocus.com, 27 Sept 2019 <https://moverfocus.com/shipping-companies/>

[16] “Top 10 Box Port Operators 2019.”

[17] Joanna Kakissis, “Chinese Firms Now Hold Stakes in Over A Dozen European Ports,” National Public Radio, 9 Oct 2018 <https://www.npr.org/2018/10/09/642587456/chinese-firms-now-hold-stakes-in-over-a-dozen-european-ports>

[18] “COSCO Shipping Ports Signs Concession Agreement with Port of Zeebrugge Reach MOU with CMA for Strategic Partnership,” press release, COSCO Shipping, 23 Jan 2018 <https://ports.coscoshipping.com/en/Media/PressReleases/content.php?id=20180123>

[19] “Port of Zeebrugge 2019:14.2% Growth” Port of Zeebrugge, 1 July 2020 <https://portofzeebrugge.be/en/news-events/port-zeebrugge-2019-142-growth> and Gavin van Marie, “Cosco Launces Move to Make Zeebrugge its North European Hub,” 01 May 2010 <https://theloadstar.com/cosco-launches-bid-to-make-zeebrugge-its-north-european-hub/>

[20] J Jonathan Hillman, “Influence and Infrastructure: The Strategic Stakes of foreign Projects,” CSIS Reconnecting Asia Project, Jan 2019, p. 9; Jones and Veit, p. 13; and Ferrai and Tei, p. 11.

[21] Ferrai and Tei, p.2.

[22] Hillman, p. 19.

[23] Gresh, p. 122.

[24] “Pakistan OKs PSA International’s Exit from Gwadar,” 01 Feb 2012, <https://www.joc.com/port-news/terminal-operators/psa-international/pakistan-oks-psa-internationals-exit-gwadar-port_20130201.html>

[25] Gresh, p. 123.

[26] “Pakistan Attack: Gunmen Storm Five-star Hotel in Balochistan,” 12 May 2019, <https://www.bbc.com/news/world-asia-48238759>

[27] “’Chinese Colony; in CPEC-Hub Gwadar Draw the Ire of People in Balochistan, Pakistan,” The EurAsian Times, 15 Dec 2020 <https://eurasiantimes.com/chinese-colony-in-cpec-hub-gwadar-draws-the-ire-of-people-in-balochistan-pakistan/>

[28] Robert Blackwill and Jennifer Marris, War by Other Means: Geoeconomic and Statecraft. Cambridge, Massachusetts: Harvard University Press, 2016, p.6.

[29] Hillman, p. 4.

[30] Logan Pauley and Hamza Shad, “Gwadar: Emerging Port City of Chinese Colony,” The Diplomat, 5 Oct 2018, <https://thediplomat.com/2018/10/gwadar-emerging-port-city-or-chinese-colony/>

[31] Jones and Veit, p. 21

[32] Gresh, pp. 66-7.

[33] USS Mitscher Public Affairs, “USS Mitscher Departs Piraeus, Greece,” 17 Apr 2019, <https://www.c6f.navy.mil/Press-Room/News/Article/1816242/uss-mitscher-departs-piraeus-greece/>

[34] Jones and Veit, p. 10.

[35] Hillman, p. 2.

[36] President United Nations Security Council, Note S/2019/691, 30 Aug 2019.

[37] US Attorney’s Office, Southern District of New York, “U.S. Government Seized Oil Tanker Used to Violate U.S. and U.N. Sanctions Against North Korea,” 23 Apr 2021, <https://www.justice.gov/usao-sdny/pr/us-government-seizes-oil-tanker-used-violate-us-and-un-sanctions-against-north-korea>

[38] Kenneth Katzman, “Iran Sanctions,” Congressional Research Service, 18 Nov 2020, pp. 10-11.

[39] Katzman, p. 8.

Featured Image: Chinese trucks carrying trade goods are pictured parked at the Gwadar port, Pakistan. (Photo via AAMIR QURESHI/AFP/Getty Images)